- You are here:

-

Home

-

Technologies & Products

- New Mobile Point-of-Sale Platform “Swiff” energizes the Mobile Payment Industry

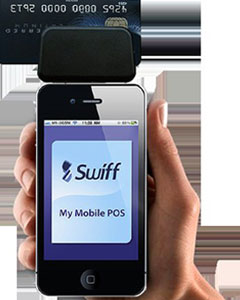

Swiff, a mobile payment platform that uses a plug-in device to transform smartphones and tablets into credit card/debit card terminals will launch its solution officially this week in Singapore.

Swiff, a mobile payment platform that uses a plug-in device to transform smartphones and tablets into credit card/debit card terminals will launch its solution officially this week in Singapore.

Jerome Cle, CEO and Founder, and Etienne Van, COO, will present and comment on the business and technology behind their innovation at a media invite at the first restaurant in Singapore that test-drives their new technology, besides providing insights on the mobile payment market in Singapore, the region and around the world.

Swiff is revolutionary in that sense that the mobile payment platform enables banks to acquire and retain market share in an increasingly competitive environment, while providing merchants with a fast and affordable way to implement credit card payment facilities. All parties involved in the payment process – merchants, customers and banks alike - will benefit from Swiff’s end-to end security that not only offers protection of credit card data, but also the reduction of fraud in payment transactions.

Replacing traditional credit card terminals, businesses now have the flexibility to secure credit card payments with their mobile phones anytime, anywhere. With real-time processing on the move, collecting payment is no longer confined to the back of the counter, which improves customer service and reduces waiting time. In general it seems as if Swiff comes at the right time for the mobile payment industry, which is expected to hit US$900 billion globally by 2014.

Easy to use

Swiff allows merchants to capture credit card payments from Visa, Mastercard, American Express, Diners and JCB and its application supports iPhone, iPod touch, iPad, Android and Tablet computers.

Merchants who sign-up to the mobile solution receive a card reader from Swiff that is plugged into the audio jack of a variety of mobile devices, allow them to accept instant credit card payments - actually similar to Square. But what sets Swiff apart from Square is its business model that permits merchants to choose from any acquiring bank of their choice to obtain the most competitive rates, since it is not a close loop solution. It is just an enabler to facilitate the payment transaction what makes it more flexible and appealing to merchants. The banks will have direct relationship with the merchant and therefore, merchants have the flexibility to plan their businesses.The merchant can swipe or manually input the credit card (Visa, Mastercard, American Express, Diners and JCB) details of the customer, capture a digital signature on the screen, and authorize a transaction.

Security guaranteed

Security measures always have priority since they are crucial to credit card transactions, and Swiff has, of course, precautionary measures is place to guarantee necessary security. The service provider makes sure that credit card data is encrypted in the reader and that only an encrypted format is sent to the gateway for payment processing, all according to the standard procedure, but on top, data is never available on the application to ensure a full end-to-end security. And of course each password and pin is allocated to one merchant and synchronized with the card-reader and the device.

Actually I was already waiting for such a mobile payment solution for a long time and now I am curious how Swiff will perform in the fast-paced and extremely competitive mobile commerce industry.

By Daniela La Marca