- You are here:

-

Home

-

Research, Analysis & Trends

- Capgemini World Payment Report 2012: E- and M-Payments continue to grow especially in Asia Pacific

For the eighth time, Capgemini‘s World Payment Report provides valuable figures and forecasts, and we‘ve attempted to pick out the highlights we thought might interest our readers most.

For the eighth time, Capgemini‘s World Payment Report provides valuable figures and forecasts, and we‘ve attempted to pick out the highlights we thought might interest our readers most.

The global volume of non-cash payments continues to show healthy growth, with the largest gain in volumes occurring in developing markets. Volumes grew by 7.1% to reach 283 billion in 2010, the most recent year for which official final data is available for all regions. Volumes jumped 16.9% in developing markets, boosted by an increase of more than 30% in both Russia and China. That growth far outpaced the modest increase in volumes in developed markets, which were still suffering the effects of the financial and economic crisis. Even in developed markets, though, the growth in non-cash payments volumes, at 4.9%, outpaced the rate of growth in gross domestic product (GDP), and developed markets still accounted for about 80% of all non-cash payments transactions globally.

Debit cards and credit cards are still the biggest driver of non-cash payments volumes globally, accounting for 55.8% of all non-cash payments in 2010, up from 53.4% in 2009 and 35.3% in 2001. Debit cards alone contributed more than one in three of all payments, partly as the use of cards for smaller-ticket transactions becomes more widespread. The aggregate use of checks continues to decline, while the outright volume of credit transfers and direct debit transactions increases, though the relative usage of these instruments is gradually declining compared to cards.

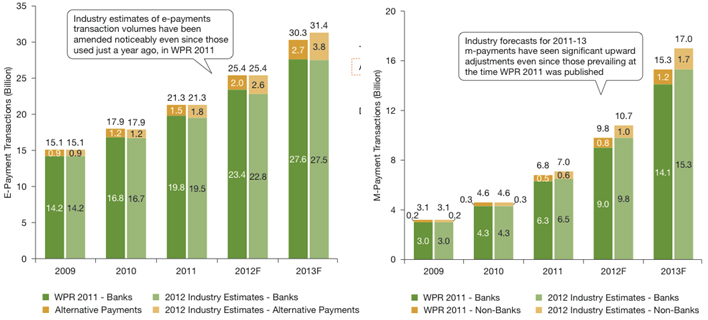

Electronic and mobile payments maintain their rapid growth trajectory. Industry estimates show the number of online payments for e-commerce activities (e-payments) is forecast to reach 31.4 billion in 2013. Analysts believe the number of payments using mobile devices (m-payments) could grow even faster, by 52.7% a year to reach 17 billion in 2013, which is faster even than the rates being forecast just a year ago.

Widespread innovation in customer-focused m-payments solutions, especially by non-banks, is rising to meet the growing demand. With these markets growing so rapidly, there is a mounting need for central banks to make sure reliable market data is being collected and monitored with the same rigor for emerging payment channels as for legacy instruments.

Asia-Pacific: Home to three of the ten largest non-cash payments markets in the world

South Korea, Japan, and Australia are among the world’s ten largest non-cash payments markets (5th, 7th, and 9th, respectively). While each market is different, they all share some common prevailing trends: especially the rising use of cards and persistent payments innovation.

A few facts offer a taste of each market:

South Korea

- Well-developed non-cash payments markets—244 transactions per inhabitant in 2010.

- Volume growth strong nevertheless—up 13.7% to reach 11.9 billion in 2010.

- Cards accounted for 60% of total volumes in 2010. In cards segment:

Japan

- Non-cash payments volumes up 11.9% to 8.5 billion transactions in 2010; usage still relatively low for a developed market (67 non-cash transactions per inhabitant in 2010).

- Credit cards accounted for 81% of total 2010 volume.

- Payment Services Act (2010) is promoting competition and innovation by allowing non-banks to provide funds transfer services that were previously restricted to banks.

- Payments-infrastructure improvements ongoing; ISO20022 message standards implemented in retail payment system in 2011.

- Osaifu-Keitai (‘Wallet Mobile’), developed by NTT DoCoMo, is now the de facto standard m-payment system, allowing consumers to use phones as substitute for cash/cards at vending machines and merchant POS. Range of payment services include e- money, identity card, loyalty card, public transport ticketing (railways, buses, air travel), and credit card.

Australia

- Non-cash payments market highly developed—283 transactions per inhabitant in 2010, among the highest in the world.

- 6.3 billion non-cash transactions in 2010, up 8.3%, cards accounted for 61% of all transactions in 2010; next most popular instrument, credit transfers, accounted for 24%.

- Payment system still evolving; moving away from bilateral clearing and setting up hub infrastructures that will enable future growth.

- The Reserve Bank of Australia’s Payments System Board is reviewing the payment systems; eyeing areas where stakeholders and regulators can cooperate to promote innovation, and open the market to newcomers.

Electronic and mobile payments continue to grow at pace

Looking ahead, industry analysts expect both the e- and m-payment segments to grow broadly, as customers increasingly embrace these alternative means and innovative solutions continue to proliferate. Industry estimates suggest the proportion of transactions handled outside bank payments systems, while small in absolute terms, is expected to grow very rapidly (see Figures 1.7 and 1.8), especially in m-payments where mobile network operators (MNOs), and mobile app stores are processing a significant number of transactions that might otherwise be handled by banks.

As mentioned, the number of e-payments is forecast to reach 31.4 billion in 2013, after sustained growth of 20 % a year in 2009-13 (see Figure 1.7). This increase is being driven by the rapid growth in alternative payment channels, and reflects the rising use by bricks-and-mortar merchants of fully functioning e-commerce capabilities, adding to the transactions volumes generated by large web retailers. E-commerce, driven by innovation in many cases, combining with bricks-and-mortar commerce can lead to the need for an integrated customer experience, including issuers, online stores, and physical merchants.

A cornerstone of long-term success for online payment services is safety and security for end-users. That’s a crucial fact that has to be considered, since there is not only a sharp rise in the number of mobile subscribers globally, but the number of m-payments are growing even faster than e-payments, too - by 52.7% a year in 2009-13 to reach 17 billion in 2013 (see Figure 1.8).

The number of m-payments users worldwide is likely to surpass more than 212 million, up from 160 million last year with mobile transaction values reaching around US$170 billion – up more than 60 percent compared to last year.

The mobile payments market has without doubt a vast potential for additional growth, although it is expected that it will experience fragmented services and solutions for the next two years, with technology providers that have to cater their solutions to local markets with different access technologies, business models and partners, under different regulatory conditions. (Source: www.capgemini.com)

By MediaBUZZ